Estate planning is an essential process that allows individuals to ensure their assets are distributed according to their wishes after their death or incapacitation. It involves creating legal documents, making important decisions, and considering the needs of loved ones. By engaging in estate planning, individuals can effectively manage and minimize estate taxes, gift taxes, and other tax impacts, while also providing peace of mind for themselves and their family.

In this comprehensive guide, we will walk you through the necessary steps and considerations involved in estate planning. From creating an inventory of your assets to reviewing beneficiaries and understanding tax laws, this guide will provide you with the knowledge and tools to embark on the estate planning journey. Whether you are a baby boomer preparing for the future or someone interested in securing their legacy, this guide will help you navigate the complexities of estate planning with empathy and clarity.

Table of Contents

- Introduction to Estate Planning

- Step 1: Create an Inventory of Your Assets

- Step 2: Account for Your Family’s Needs

- Step 3: Establish Your Directives

- Step 4: Review Your Beneficiaries

- Step 5: Understand State Estate Tax Laws

- Step 6: The Value of Professional Help

- Step 7: Plan to Reassess

- Additional Considerations for Baby Boomers

- Estate Planning Tools and Resources

- Common Mistakes to Avoid in Estate Planning

- Conclusion

1. Introduction to Estate Planning

Estate planning is a proactive approach to managing your assets and ensuring their proper distribution upon your death or incapacitation. It involves creating legal documents such as wills, trusts, powers of attorney, and living wills, among others. These documents outline your wishes and provide instructions for your loved ones and designated representatives to follow.

The primary goal of estate planning is to minimize uncertainties and potential conflicts among family members while maximizing the value of your estate. It allows you to have control over who receives your assets, who will make decisions on your behalf, and how your affairs will be managed in the event of your incapacitation or death.

2. Step 1: Create an Inventory of Your Assets

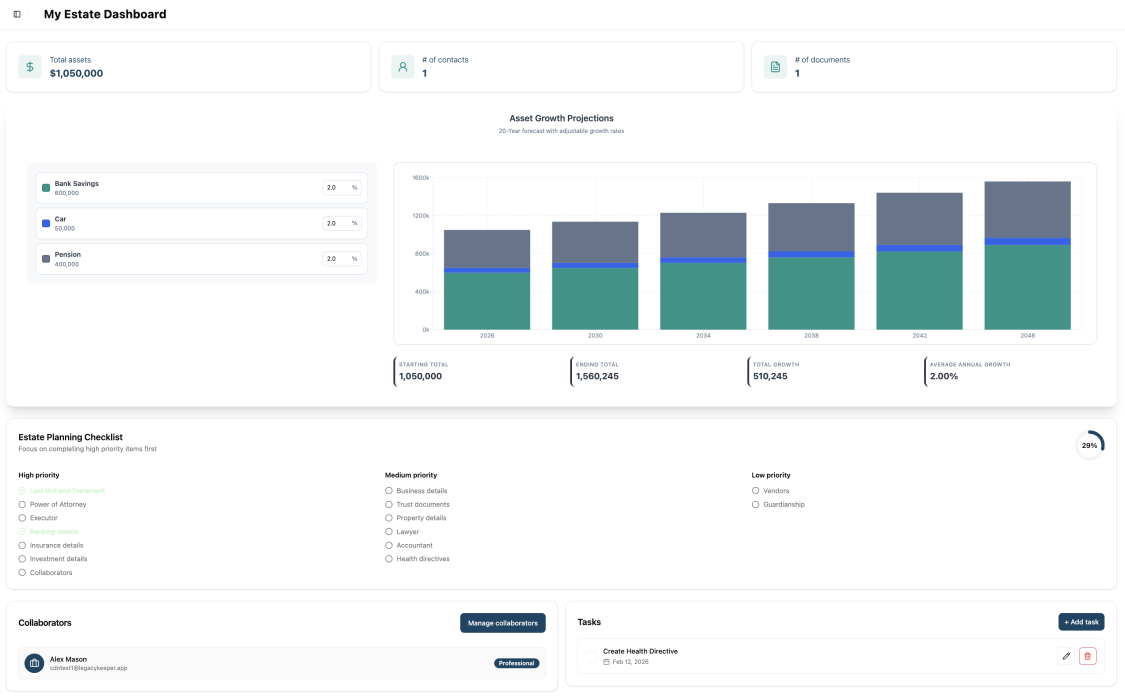

Before diving into the specifics of estate planning, it is important to have a comprehensive understanding of your assets. Creating an inventory will help you identify and organize your tangible and intangible assets. This includes homes, vehicles, financial accounts, retirement plans, life insurance policies, and any personal possessions of value.

Tangible Asset

Tangible assets are physical items that hold monetary or sentimental value. These may include:

- Real estate properties such as homes, land, or vacation properties.

- Vehicles like cars, motorcycles, or boats.

- Collectibles such as artwork, antiques, or coins.

- Personal possessions like jewelry, furniture, or family heirlooms.

Intangible Assets

Intangible assets are non-physical assets with financial value. These may include:

- Bank accounts, including checking, savings, and certificates of deposit.

- Investments such as stocks, bonds, mutual funds, or retirement accounts.

- Life insurance policies and annuities.

- Ownership in a business or intellectual property.

By creating a comprehensive inventory of your assets, you will have a clear picture of what needs to be included in your estate plan. This will serve as a foundation for making informed decisions regarding the distribution of your assets.

3. Step 2: Account for Your Family’s Needs

When planning your estate, it is crucial to consider the needs and circumstances of your family members. This includes identifying dependents, minor children, and individuals with special needs who may require ongoing care and support. Taking these factors into account will ensure that your estate plan provides for their well-being and protection.

Naming a Guardian for Minor Children

If you have minor children, it is important to name a guardian who will assume responsibility for their care in the event of your death. This decision should be made carefully, taking into consideration the guardian’s ability to provide a loving and stable environment for your children.

Additionally, you may also want to designate a trustee who will manage any assets or funds left to your children until they reach a certain age or milestone. This will ensure that their financial needs are met while they are under the care of the appointed guardian.

Providing for Dependent Family Members

In addition to minor children, you may have other dependent family members who rely on your support. This could include elderly parents, disabled siblings, or other individuals for whom you are the primary caregiver. Consider their financial and emotional needs when creating your estate plan, ensuring that they will be taken care of in the event of your absence.

4. Step 3: Establish Your Directives

Establishing your directives involves making important decisions regarding medical care, end-of-life wishes, and the management of your financial affairs. By clearly outlining your preferences, you can ensure that your wishes are respected and that your designated representatives have the necessary authority to act on your behalf.

Creating a Last Will and Testament

A last will and testament is a legal document that outlines how you want your assets to be distributed after your death. It allows you to name beneficiaries, designate an executor to carry out your wishes, and specify any special requests or conditions.

Without a valid will, your assets will be distributed according to state laws, which may not align with your intentions. By creating a will, you maintain control over the distribution of your assets and provide clarity for your loved ones during a difficult time.

Exploring Living Trusts

In addition to a will, you may want to consider establishing a living trust. A living trust is a legal entity that holds your assets during your lifetime and allows for their seamless transfer to your beneficiaries upon your death. Creating a living trust can help avoid the probate process, which can be time-consuming and costly.

Unlike a will, a living trust provides privacy as it does not become part of the public record. It also allows for more flexibility and control over the distribution of your assets. Consult with an attorney to determine if a living trust is suitable for your estate planning needs.

Advance Directives and Medical Care

Advance directives, such as a living will and healthcare power of attorney, allow you to express your medical care preferences and designate a trusted individual to make decisions on your behalf if you are unable to do so. These documents ensure that your healthcare wishes are respected and that your loved ones are empowered to act in your best interest.

A living will outlines your preferences for medical treatments, end-of-life care, and the use of life-sustaining measures. It provides guidance to healthcare professionals and ensures that your wishes are followed, even if you are unable to communicate them.

A healthcare power of attorney designates a trusted individual, often referred to as a healthcare proxy or agent, to make medical decisions on your behalf when you are unable to do so. This person should be someone who understands your values, beliefs, and medical preferences.

Powers of Attorney for Financial Affairs

In addition to healthcare decisions, it is important to designate someone to handle your financial affairs if you become incapacitated. A durable power of attorney allows you to appoint a trusted individual to manage your financial matters, pay bills, file taxes, and make other financial decisions on your behalf.

Consider selecting someone who is financially responsible and capable of handling these responsibilities. It is also possible to appoint different individuals for healthcare and financial powers of attorney, depending on their respective expertise.

5. Step 4: Review Your Beneficiaries

As life circumstances change, it is essential to regularly review and update your beneficiaries to ensure that your assets are distributed according to your current wishes. Failing to update your beneficiaries can result in unintended consequences and assets being allocated to individuals who may no longer be a part of your life.

Review the beneficiaries listed on your retirement accounts, life insurance policies, and any other accounts or assets that allow for beneficiary designations. Consider any changes in relationships, births, deaths, or divorces that may require updates to your beneficiary designations.

Additionally, ensure that the contact information for your beneficiaries and designated representatives is up to date. This will help facilitate a smooth transition of assets and ensure that your loved ones are aware of their roles and responsibilities.

6. Step 5: Understand State Estate Tax Laws

When planning your estate, it is important to consider the estate tax laws of your state. Estate taxes are imposed on the value of an estate upon an individual’s death, and the thresholds and rates vary from state to state.

It is essential to understand your state’s estate tax laws to determine if your estate may be subject to taxation. Consult with an attorney or tax professional who specializes in estate planning to ensure that you are aware of any potential tax obligations and to explore strategies for minimizing estate taxes.

7. Step 6: The Value of Professional Help

While it is possible to create a basic estate plan on your own, seeking professional help can provide valuable guidance and ensure that your estate plan is comprehensive and legally sound. Estate planning attorneys, financial advisors, and tax professionals can offer expertise and assistance in navigating complex legal and financial matters.

By working with professionals who specialize in estate planning, you can ensure that your wishes are properly documented, your assets are protected, and your estate plan aligns with your overall financial goals. They can also provide ongoing advice and support as your circumstances and goals evolve over time.

8. Step 7: Plan to Reassess

Estate planning is not a one-time event but an ongoing process. As life circumstances change, it is important to revisit and reassess your estate plan regularly. This includes reviewing and updating your legal documents, beneficiary designations, and directives to ensure that they reflect your current wishes.

Significant life events such as marriage, divorce, the birth of a child, or the death of a loved one may necessitate revisions to your estate plan. Regular reassessment will help ensure that your plan remains relevant and effective in achieving your goals.

9. Additional Considerations for Baby Boomers

Baby boomers, individuals born between 1946 and 1964, face unique considerations and challenges when it comes to estate planning. As this generation ages, it becomes increasingly important to plan for the future and the potential need for assistance from loved ones.

Long-Term Care Planning

Long-term care planning is a crucial aspect of estate planning for baby boomers. Consider the potential need for assisted living, nursing home care, or in-home care as you age. Explore options such as long-term care insurance or Medicaid planning to ensure that you have the necessary resources to meet your care needs.

Communicating with Loved Ones

Open and honest communication with your loved ones is essential when it comes to estate planning. Discuss your wishes, intentions, and the responsibilities of designated representatives with your family members. This will help avoid confusion and potential conflicts in the future, ensuring that your estate plan is carried out smoothly.

Organizing Important Documents

Gather and organize important documents such as wills, trusts, powers of attorney, insurance policies, and financial account information. Store them in a secure location and ensure that your designated representatives know where to find them in the event of your incapacitation or death.

By taking these additional considerations into account, baby boomers can approach estate planning with a comprehensive understanding of their needs and the needs of their loved ones.

10. Estate Planning Tools and Resources

Several tools and resources are available to assist you in the estate planning process. These include online services, software programs, and professional advisors who specialize in estate planning. Here are a few popular options:

-

Online Will Services: Online platforms offer interactive questionnaires and templates to help you create a legally binding will specific to your state’s laws. Examples include Trust & Will, Nolo’s Quicken WillMaker, and LegalZoom.

-

Estate Planning Software: Software programs provide comprehensive tools for creating and managing your estate plan. These programs often include features such as document templates, asset inventories, and legal guidance. Examples include Quicken WillMaker & Trust and Everplans.

-

Professional Advisors: Estate planning attorneys, financial advisors, and tax professionals can provide personalized guidance and expertise to help you navigate the complexities of estate planning. They can ensure that your estate plan aligns with your unique circumstances, goals, and legal requirements.

When choosing a tool or resource, consider your comfort level with technology, the complexity of your estate, and your need for professional advice. It is important to select an option that best suits your individual needs and preferences.

11. Common Mistakes to Avoid in Estate Planning

While estate planning is a critical process, it is not uncommon for individuals to make mistakes that can lead to unintended consequences or legal challenges. Here are some common mistakes to avoid:

Procrastination

Procrastinating on estate planning can have significant consequences. It is important to start the process as soon as possible to ensure that your wishes are documented and legally binding. Putting off estate planning can leave your loved ones in a difficult position and may result in your assets being distributed according to state laws rather than your intentions.

Failure to Update Beneficiaries

Failing to review and update beneficiary designations can lead to assets being distributed to individuals who are no longer part of your life or do not align with your current wishes. Regularly review and update your beneficiaries to reflect changes in relationships, births, deaths, or divorces.

Lack of Communication

Failing to communicate your estate plan and intentions with your loved ones can lead to confusion and potential conflicts. Openly discuss your wishes, responsibilities, and the role of designated representatives with your family members to ensure a smooth transition and understanding of your estate plan.

Overlooking Digital Assets

In today’s digital age, it is important to consider your digital assets when planning your estate. This includes online accounts, email, social media profiles, and digital files. Create a list of your digital assets and provide instructions for their management and transfer to your designated representatives.

Neglecting to Reassess and Update

Estate planning is an ongoing process that requires regular reassessment and updates. Failing to review and update your estate plan can result in outdated or ineffective documents. Regularly revisit your estate plan to ensure that it reflects your current wishes, circumstances, and legal requirements.

Avoiding these common mistakes will help ensure that your estate plan is comprehensive, legally sound, and aligned with your wishes.

12. Conclusion

Estate planning is a proactive and essential process that allows individuals to protect their assets, provide for their loved ones, and ensure their wishes are carried out. By following the steps outlined in this guide and considering the specific needs of your family, you can create a comprehensive estate plan that brings peace of mind and prepares you for the future.

Remember, estate planning is not a one-time event but an ongoing process. Regularly reassess and update your estate plan to reflect changes in your life circumstances, relationships, and goals. Seeking professional help and utilizing available resources can provide valuable guidance and support throughout the estate planning journey.

Take control of your future and start estate planning today. By doing so, you are securing a legacy that will provide for your loved ones and bring peace of mind for years to come.