Introduction

As a Baby Boomer approaching retirement age, it is increasingly important you to plan for the future and ensure that your assets are properly managed and distributed. Estate planning is a crucial step in this process, as it allows individuals to determine how your belongings and property will be handled by your dependents. In this comprehensive guide, we will outline the essential steps to prepare your estate and provide valuable insights for you to navigate this complex process effectively.

Step 1: Taking Inventory of Your Assets

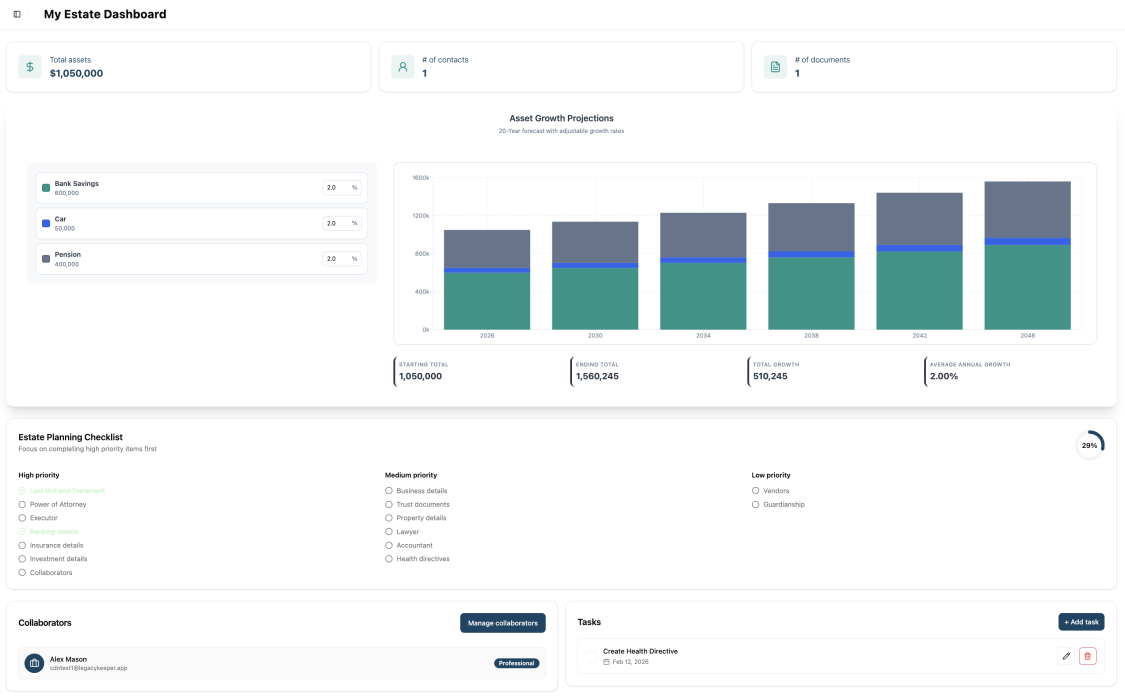

Before you can begin the estate planning process, it is essential to take inventory of all your assets. This includes both tangible and intangible possessions such as homes, vehicles, bank accounts, retirement accounts, investments, and personal belongings. Creating a comprehensive list will help you make informed decisions about how to distribute your assets and ensure that nothing is overlooked.

To simplify this process, you can categorize your assets into different sections, such as:

Tangible Assets

-

Real Estate: List all properties you own, including your primary residence, vacation homes, and rental properties.

-

Vehicles: Include cars, motorcycles, boats, or any other vehicles registered under your name.

-

Personal Belongings: Take note of valuable collectibles, jewelry, artwork, antiques, and other significant personal possessions.

Intangible Assets

-

Financial Accounts: Compile information about your checking and savings accounts, certificates of deposit, stocks, bonds, mutual funds, and retirement accounts.

-

Insurance Policies: Make a record of life insurance policies, including the names of beneficiaries.

-

Business Ownership: If you own a business, document your ownership interest and any relevant details.

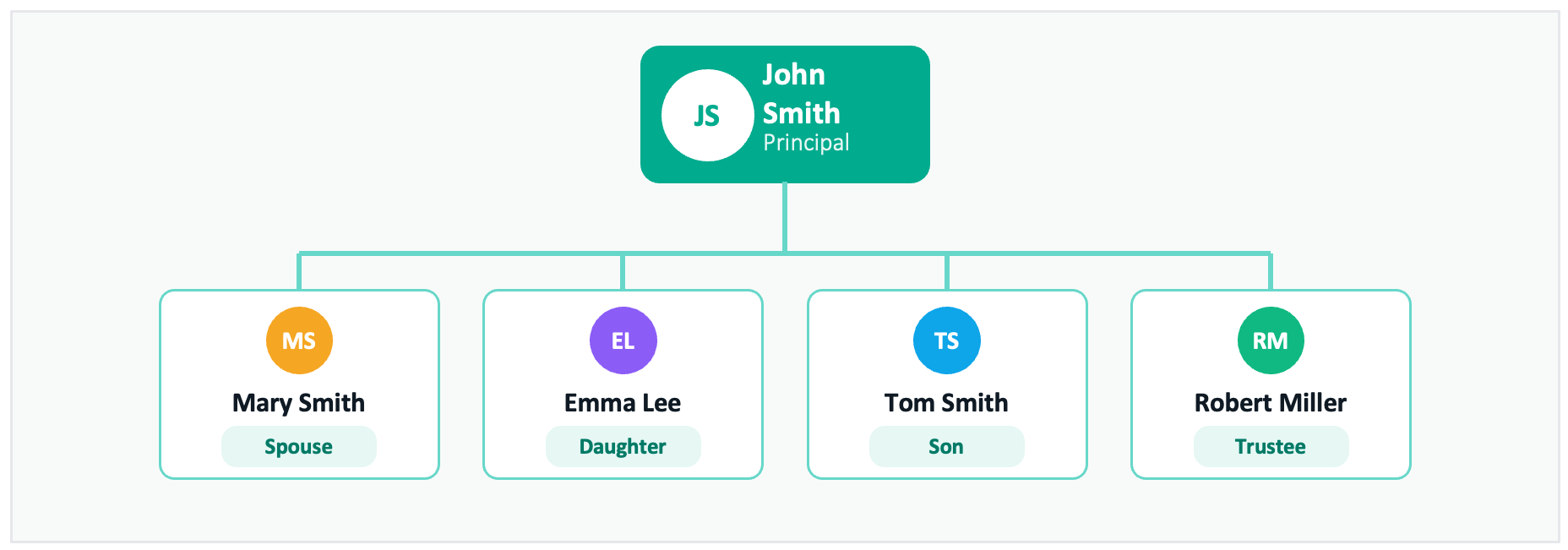

Step 2: Creating a Last Will and Testament

A last will and testament is a crucial document that outlines your final wishes regarding the distribution of your assets. It enables you to designate beneficiaries and appoint an executor who will oversee the administration of your estate. Without a will, your assets may be subject to probate, a legal process that can lead to unintended outcomes.

When creating your will, consider the following:

- Naming an Executor: Choose a trusted individual who will be responsible for managing your estate and carrying out your wishes.

- Distribution of Assets: Clearly state how you want your assets to be distributed among your beneficiaries.

- Guardianship for Minor Children: If you have underage children, designate a guardian who will be responsible for their care in the event of your passing.

Remember to periodically review and update your will to reflect any significant life changes, such as births, deaths, marriages, or divorces within your family.

Step 3: Establishing a Living Trust

In addition to a will, you may also consider establishing a living trust as part of your estate plan. A living trust allows you to transfer assets into a trust during your lifetime, which can help avoid probate and provide greater control over the distribution of your assets.

Here are some key points to consider when setting up a living trust:

- Trustee Selection: Choose a trustee who will manage the trust and carry out your instructions.

- Funding the Trust: Transfer ownership of your assets into the trust, including real estate, financial accounts, and other valuable properties.

- Successor Trustees: Designate successor trustees who will assume control if the original trustee becomes unable or unwilling to fulfill their duties.

Consulting with an attorney specializing in estate planning can provide valuable guidance and ensure that your living trust is properly executed.

Step 4: Appointing a Power of Attorney

A power of attorney (POA) is a legal document that appoints an individual to act on your behalf in financial or medical matters if you become incapacitated. This designated person, known as the attorney-in-fact, can make decisions and manage your affairs according to your instructions.

There are different types of POAs to consider:

- Durable Power of Attorney: This type of POA remains in effect even if you become incapacitated and allows your attorney-in-fact to handle financial and legal matters on your behalf.

- Medical Power of Attorney: Also known as a healthcare power of attorney, it grants someone you trust the authority to make medical decisions on your behalf if you are unable to do so.

It is important to select individuals who are responsible, trustworthy, and capable of making decisions in your best interests. Consider discussing your intentions with the appointed individuals to ensure they understand your wishes.

Step 5: Drafting a Living Will

A living will, also known as an advance healthcare directive, allows you to outline your preferences for medical treatment in the event that you become unable to communicate your wishes. This document ensures that your healthcare decisions align with your values and beliefs.

When creating a living will, consider the following:

- Life-Prolonging Treatments: Specify your preferences regarding life-sustaining treatments, such as artificial respiration, tube feeding, or resuscitation.

- Palliative Care: Indicate your desire for pain management and other supportive measures to enhance your comfort.

- Organ Donation: Express your wishes regarding organ and tissue donation.

Sharing your living will with your healthcare power of attorney ensures that your appointed agent understands and can advocate for your medical preferences.

Step 6: Considering Estate Tax Obligations

Familiarize yourself with the estate tax laws at both the federal and state levels to understand any potential tax implications for your estate. The federal estate tax applies only to larger estates, exceeding a specific threshold, while some states may have their own estate or inheritance taxes.

Consulting with an attorney or tax professional can help you navigate these complex tax regulations and explore strategies to minimize tax liabilities.

Step 7: Organizing Your Digital Assets

In the digital age, it is essential to consider your digital assets when preparing your estate. These assets include online accounts, digital files, social media profiles, and cryptocurrency holdings. Failure to account for these assets can result in their loss or misuse after your passing.

To organize your digital assets effectively, consider the following:

- Compile a List: Create a comprehensive list of all your online accounts, including usernames and passwords.

- Appoint a Digital Executor: Designate someone you trust to manage and distribute your digital assets according to your wishes.

- Secure Your Information: Safely store your login credentials and instructions for accessing your digital assets, while ensuring the security of sensitive information.

By including digital assets in your estate plan, you can protect your online presence and ensure that your loved ones have access to important information.

Step 8: Creating a Guide for Your Executors

To facilitate the administration of your estate, consider creating a guide for your executors. This guide should provide detailed information about your assets, debts, and final wishes, making it easier for your executors to fulfill their responsibilities.

Include the following information in your executor’s guide:

- Financial Accounts: List all bank accounts, investment portfolios, and other financial assets, along with contact information for financial institutions.

- Insurance Policies: Document all life insurance policies, including policy numbers and contact information for insurance providers.

- Debts and Liabilities: List any outstanding debts, loans, mortgages, or other financial obligations.

- Funeral and Burial Instructions: Clearly state your preferences for funeral arrangements, burial or cremation, and any specific requests.

By providing this comprehensive guide, you can alleviate the burden on your executors and ensure that your final wishes are carried out efficiently.

Step 9: Regularly Reviewing and Updating Your Estate Plan

An estate plan is not a one-time endeavor but rather an ongoing process. Life circumstances change, and it is crucial to review and update your estate planning documents periodically to reflect these changes accurately.

Consider the following scenarios that may warrant revisiting your estate plan:

- Births or Deaths: If you have children or experience the loss of a loved one, it is essential to update your estate plan to reflect these changes.

- Marriages or Divorces: Changes in marital status often necessitate revisions to your beneficiary designations and distribution plans.

- Financial Changes: Significant changes in your financial situation, such as the acquisition or sale of assets, may require adjustments to your estate plan.

Regularly consulting with an attorney or estate planning professional can help ensure that your estate plan remains up to date and aligned with your current circumstances.

Conclusion

Preparing your estate is a critical responsibility, especially for baby boomers approaching retirement age. By following these essential steps and seeking professional guidance when necessary, you can create a comprehensive estate plan that protects your assets, ensures your final wishes are respected, and provides peace of mind for you and your loved ones.

Remember, estate planning is a personal and intricate process, and it is crucial to tailor your plan to your unique circumstances. By taking the time to prepare your estate properly, you can leave a lasting legacy that reflects your values and provides for future generations.

Leave a Reply